- This past weekend, global markets received another sudden economic shock. Saudi Arabia announced it will engage in an oil price war with Russia after Vladimir Putin refused to join an OPEC agreement. Oil prices collapsed about 20% on the news, which will have a large ripple effect throughout the global economy. While lower gasoline prices will benefit consumers, energy companies’ earnings and dividends will be negatively impacted.

- Bond yields have also fallen, with the yield on the 10-year U.S. Treasury Note dropping to 0.44% amid demand for safer bonds and the likelihood of lower interest rates.

- In an effort to stimulate economic demand, we now expect that the Federal Reserve will cut short-term rates further when the Federal Open Market Committee meets later in March.

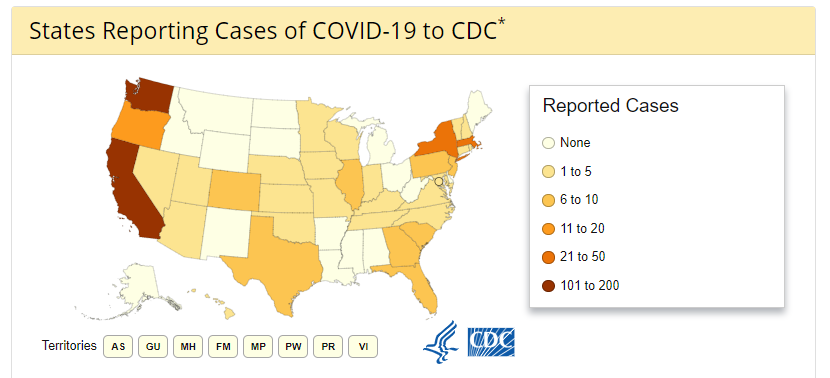

- While the most severe economic impact will be felt in countries most vulnerable to the spread of the disease, the ability of the U.S. healthcare system and the private sector to cope with the virus will be a critical factor in mitigating the economic impact over time.

- We see an increasing probability of a recession in the U.S. this year, as multiple industries and companies experience falling demand and financial distress resulting from the spread of COVID-19.

What is our current outlook?

No one has a crystal ball, but if we were to state our base case outlook, here is what we believe is reasonable to expect:

- Virus: The virus is likely to spread further in the U.S., but we expect an improving response in containing its spread over the coming weeks and months. We anticipate a vaccine within 15-18 months and antiviral medication (reducing severity of symptoms, not a cure) within 6 months.

- Oil price: The price will take time to find an equilibrium level where supply and demand are in balance. We believe that the price will ultimately be higher than today’s level. As the latest decision by Saudi Arabia to drive oil prices lower is more politically than economically driven, we could be in a low price environment longer than would otherwise be the case. Prices in the $30-$40 range are low enough to cause significant stress for marginal producers of oil, which includes the U.S in general. Energy companies make up a small part of the U.S. Equity portion of client portfolios and most of our client holdings are in integrated companies that are more resilient during times of low commodity prices.

- US Stock Market: We foresee 2-3 quarters of dampened economic activity with activity gradually improving thereafter. In other words, a relatively short-lived downturn. This bodes well for staying invested in stocks, while avoiding panic selling.

What do we recommend?

While the current situation feels unnerving, we remind you that the markets (and the world) have experienced countless analogous periods of angst in the past, only to persevere and march ahead to new, highs. In fact, as we write this note, we are reminded of the market low exactly 11 years ago today, March 9, 2009, during the Great Recession. Fear and uncertainty reached a peak, investor selling capitulated, and markets bottomed. Since then, despite the recent market decline, the US stock market has returned 450%. These numbers remind us that patient investors who do not panic by selling at the lows have been handsomely rewarded over time. It is also important to have liquidity to meet cash obligations without the need to sell stocks at or near market bottoms. We have been asking you, and will continue to ask, about any known needs for cash over the next year.